The Psychology of Money: Why People Make Emotional Decisions

Most people understand the basics of good financial behavior. They know that saving matters, that markets fluctuate, and that long-term plans typically work better than emotional reactions. Yet many still find themselves second-guessing decisions, avoiding money conversations, or reacting strongly during uncertain times.

This disconnect isn’t about intelligence or discipline. It’s because money decisions are often about more than just numbers—they're also shaped by emotions, habits, and experiences. Recognizing these influences is the first step toward building healthier financial habits over time.

Your Money Story Shapes Your Money Habits

Financial behavior is rarely the result of one major decision. More often, it’s influenced by patterns repeated over years—spending routines, saving behavior, and reactions to market changes that develop gradually and become automatic.

These habits tend to be affected by early experiences with money: how your family talked about it (or didn’t), moments of financial stress or abundance, and lessons learned during formative years. Someone who grew up experiencing financial instability may prioritize safety above all else. Someone whose family had steady financial growth may feel comfortable with uncertainty. If your parents never discussed money, you might avoid financial conversations even when they’re urgently needed.

Understanding your personal money history helps explain why certain financial situations feel comfortable or uncomfortable to you. That self-awareness is the foundation for meaningful change.

2 Emotions That Drive Most Money Decisions

Fear is a typical reaction during times of uncertainty, such as market volatility, economic headlines, health concerns, or job transitions. Fear can lead to thoughtful caution, which is valuable. But it can also result in paralysis: avoiding investment conversations, keeping too much in cash, or postponing important decisions entirely.

Optimism often surfaces during periods of stability or growth. It fuels confidence and action, which can be productive. However, it can also lead to overconfidence—taking on excessive risk, assuming favorable conditions will continue indefinitely, or underestimating how quickly circumstances can change.

Both of these emotions can affect financial decisions, but neither is the enemy. Problems arise when decisions are made entirely from an emotional place, without considering logic or data. When that happens, choices may reflect immediate feelings while ignoring longer-term intentions.

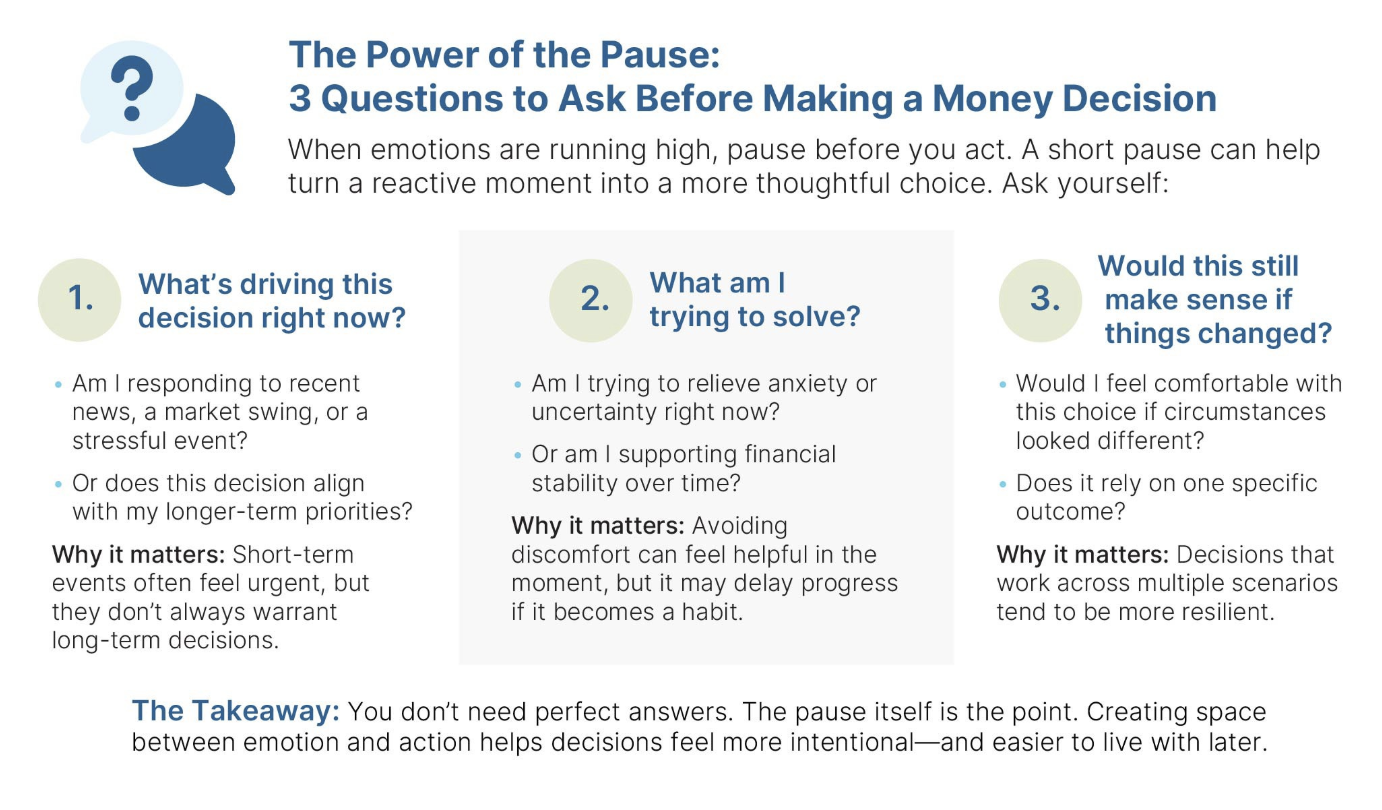

The Power of the Pause

You don’t need to eliminate emotions or analyze every purchase. But you can develop one simple habit that dramatically improves financial outcomes: pause before acting.

When you’re about to make or postpone a financial decision, ask yourself three questions:

Am I reacting to something recent or following my long-term plan? If the news cycle or a recent event is driving this decision, a 48-hour pause before acting could help put things in clearer perspective.

Am I trying to avoid short-term discomfort or build long-term security? Sometimes avoiding discomfort is wise. Other times, it’s procrastination in disguise.

Would this still make sense if circumstances changed? If your reasoning works only in one specific scenario, the decision might be too narrow.

These questions can help create a balance between impulse and action. That brief pause allows decisions to be guided by perspective rather than emotion, so they make more logical sense in the long term.

What This Looks Like in Practice

Consider someone checking their investment account daily during market volatility. Each check triggers an emotional response—anxiety when values drop, relief when they rise. Before long, they’re thinking about selling to “stop the losses” or “lock in gains.”

The pause questions help here: Am I reacting to something recent? Yes—today’s market drop. Am I avoiding discomfort or building security? Avoiding discomfort. Would this make sense if circumstances changed? If the market recovered next month, I’d regret selling.

That awareness doesn’t guarantee the “right” decision, but it helps to make a more intentional one. Maybe they decide to check their account monthly instead of daily. Maybe they reaffirm their long-term strategy. Either way, they’re responding thoughtfully rather than reacting emotionally.

A Professional Perspective

One of the most valuable aspects of working with a financial advisor isn’t just technical expertise—it’s the outside perspective. When you’re in the middle of an emotional reaction, it’s difficult to see clearly. An advisor can help separate feeling from fact, especially during major transitions or periods of volatility.

Building a Healthier Relationship with Money

A healthier relationship with money develops through understanding personal tendencies and building systems that account for real human behavior. This doesn’t mean achieving perfect rationality or never feeling anxious about money; it means recognizing patterns, creating helpful structures, and making intentional choices.

Some people benefit from automating savings so emotion doesn’t enter the equation. Others need to limit how often they check account balances. Some find it helpful to establish decision rules in advance; for example, “I won’t make investment changes based on single-day market moves” or “I’ll wait 24 hours before any purchase over $500.”

The specific strategies matter less than the underlying principle: acknowledge how psychology influences your choices, and then design systems that work with your tendencies rather than against them.

Start small. The next time you feel an urge to make a financial move, just pause. Notice how you’re feeling. Ask yourself those three questions. Then decide.

FAQs About About Financial Behavior and Decision-Making

-

Psychology plays a significant role in financial decision-making because emotions, habits, and past experiences often influence how people save, spend, invest, and react to market events. Understanding these behavioral patterns can help individuals make more intentional financial choices that align with their long-term goals.

-

A money story refers to the beliefs and attitudes about money that develop through life experiences, family influences, and financial circumstances. These experiences can shape spending habits, saving behaviors, investment decisions, and overall financial confidence. Recognizing your money story can help you identify patterns and make positive financial changes.

-

Fear can cause investors and savers to become overly cautious during periods of uncertainty. This may lead to avoiding important financial decisions, holding excessive cash, delaying investments, or making emotional reactions to short-term market fluctuations rather than focusing on long-term financial objectives.

-

While optimism can encourage positive financial action, excessive optimism may lead to taking unnecessary risks, assuming favorable market conditions will continue indefinitely, or underestimating potential challenges. A balanced approach that combines optimism with careful planning can help support long-term financial success.

-

Taking a pause before making a financial decision allows time to evaluate whether emotions are driving the choice. Asking questions about long-term goals, current circumstances, and potential outcomes can help reduce impulsive reactions and improve decision-making.

-

Investors can reduce emotional decision-making by focusing on a long-term investment strategy, limiting how often they check account balances, avoiding decisions based on daily market movements, and consulting with a financial advisor for objective guidance during periods of uncertainty.

-

A financial advisor can provide an objective perspective during emotionally charged situations, helping clients separate feelings from facts. Advisors can also help create strategies, systems, and accountability measures that support disciplined financial decisions and long-term financial goals.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG, LLC, is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright 2026 FMG Suite.

© 2026 Commonwealth Financial Network®